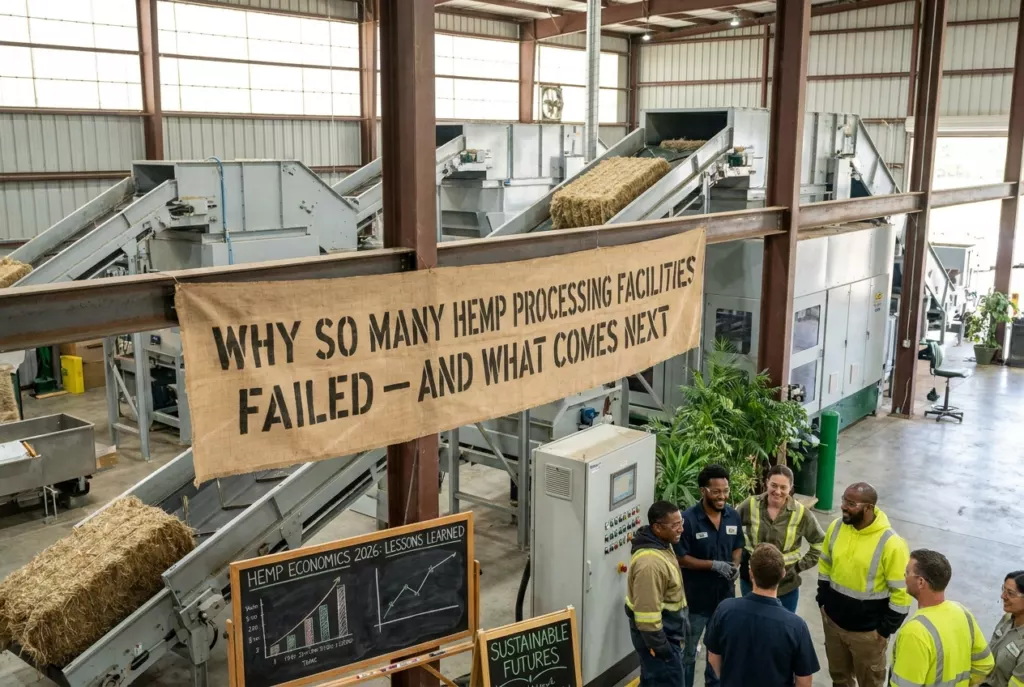

Our story opens in a converted warehouse on the edge of farm country, the smell hits you first—green stem, warm metal, a faint solvent edge if the line is built for extraction. Then the sound: conveyors, mills, separators, the confident rhythm of a plant that is supposed to turn raw hemp into something buyers can spec, bag, and repeat. For a few years after the 2018 Farm Bill reframed hemp cultivation in the United States, scenes like this multiplied on pitch decks and ribbon-cutting posts. The emotional bet was simple: if fields were suddenly legal, someone had to “add value” close to home.

The twist is how often the story jumped from ribbon cutting to quiet winter—shifts shortened, maintenance triaged, farmers told to call back when “markets improve.” The failure was rarely one villain. It was more like a pile-up—capital intensity meeting an immature demand curve, regulatory seams between what is allowed in the field and what is straightforward to sell in packaged form, and business models that assumed a commodity would behave like a mature one. This piece walks through that arc the way you would explain it across a desk at a co-op or a lenders’ conference: human stakes first, mechanics second, and a sober look at what “next” can mean without pretending the path is automatic.

How we got here

The legal story begins with cultivation rules and sampling logic, not with a processing handbook. USDA’s Agricultural Marketing Service administers the domestic hemp production program—testing, compliance, disposal of “hot” lots—because that is the lane Congress framed in farm-bill-era law; you can see the program’s public lane at USDA AMS hemp rules and resources. That clarity for growers created momentum: more hectares (and headlines) and, alongside them, a race to stand up decortication, pelletizing, cold pressing, extraction, and “seed to shelf” dreams.

Then the belt tightened. Not always in dramatic courtroom headlines—more in the grinding way supply chains tighten: contract defaults, off-quality lots, lenders asking harder questions about offtake, and buyers comparing hemp ingredients against incumbents that already had decades of logistics and specifications. In CBD-facing lanes especially, downstream uncertainty about how products may be marketed caught up with plant-level optimism; FDA’s plain-language overview of open questions for cannabis-derived ingredients in consumer products is published at FDA consumer updates on cannabis-derived products (useful context for why some ingredient stories stayed complicated, without drifting into medical claims).

Over the same years, fiber and grain narratives kept their own slower clocks—closer to equipment physics, long-sheep textile memories, and the unglamorous work of meeting spec for animal feed or specialty paper. The industry’s lesson was less “hemp failed” than “time horizons collided”: three-year money walking into ten-year infrastructure problems.

People & stakes

The grower on a spreadsheet deadline is not an aesthetic— it is a cash-flow reality. Planting decisions are seasonal; lenders and landlords are not. When a processor pushes delivery windows or renegotiates moisture and foreign-matter thresholds, the pain shows up as a quiet line on a balance sheet before it shows up in a press release.

The processor as field mechanic lives in a different timescale: depreciation schedules, insurance, maintenance techs, and utility load profiles. Hemp is greedy equipment—wear, dust, variability between cultivars and regions, and the eternal mismatch between “what the field produced” and “what the contract assumed.” A facility can be “successful” on pilot runs and still lose the year if-throughput and uptime do not meet the debt covenant math.

The brand buyer and ingredient gatekeeper often asks for what sounds boring—Certificates of Analysis, traceability, batch repeatability, indemnities—because boring is how you keep recalls and label risk out of the news. That gatekeeping is not anti-hemp; it is pro-stability.

Regulators sit at the seams. A state agriculture department may know cultivation cold while reminding you that processing and retail sit elsewhere in government—which matters when you are trying to explain why a legal crop still has awkward sales paths for certain product forms. Colorado’s public hemp program hub (cultivation-focused, with clear limits on what the agency does and does not regulate) illustrates how state portals communicate those boundaries; see Colorado Department of Agriculture hemp resources as a representative example, not the universal U.S. rulebook.

Consequences & what’s next

The human consequence is a patchwork map: towns that almost had a new payroll, regions that did get a modest anchor employer, and operators who learned harder lessons about offtake than about stainless steel. If you live near one of the quieter plants, the story looks less like “collapse” and more like hibernation—maintenance mode, selective tolling, a pivot from one product line to another as markets teach their preferences.

The more hopeful through-line—still contingent, not guaranteed—is consolidation with purpose. Smaller numbers of processors can still mean healthier throughput if they are tied to real contracts: feed mills that know the pellet spec, textile pilots that accept dirty fiber economics for what they are, ingredient buyers willing to standardize on fewer varieties. The political economy of the next chapter is less “spray and pray” volume and more “prove the run.”

Standards work mirrors that maturity shift. When processes become repeatable, banks and insurers breathe easier; volunteer standards bodies have tried to meet the industry where it is, as with ASTM’s Committee D37 on cannabis, which includes industrial-hemp-facing subcommittee work alongside other cannabis-related lanes. That is not a magic stamp—but it is a sign of the industry attempting to speak the same dialect as other adult supply chains.

A processor does not go broke because hemp is “impossible.” It goes quiet when the calendar of money arrives before the calendar of reliable buyers.

Behind the headline

Think of U.S. hemp as several industries sharing a plant name. Fiber wants decortication, grading, and often regional clustering to survive logistics. Grain and feed want cleanliness, stability, and sane comparisons to other oilseeds and roughage markets. Extract-focused infrastructure wants compliant feedstock and conservative assumptions about which product forms are straightforward to distribute under current federal and state consumer-product rules—not a verdict on cannabinoid efficacy, a business realism point.

Federal hemp production policy is only one tile in that mosaic. Trade coverage and producer education across farm programs can still be useful mirrors for how policy narratives meet county-level decisions; for a business press vantage, MJBiz Daily is one long-running trade source that has followed hemp alongside cannabis sector economics. When you read stories of facility idling, translate the adjectives into balance-sheet nouns: throughput, yield loss, energy cost, and contract law.

If you need the statutory spine in primary-text form, the congressional file for the Agriculture Improvement Act of 2018 is indexed at Congress.gov’s page for H.R.2 (115th)—helpful when separating what the law actually authorizes from what a pitch deck implies.

Verification & sources

This editorial does not cite a single national registry of “hemp processing plant closures,” because public, standardized, nationwide counts of facility-level outcomes are not consolidated the way crop acres can be tabulated in agricultural surveys. USDA’s National Agricultural Statistics Service publishes many agricultural datasets useful for macro context—see USDA NASS—but facility solvency is typically observed through local reporting, court filings, trade press, investor disclosures, and industry rumor in unequal measure.

What we treat as well supported here: the existence and public description of federal hemp production oversight under USDA AMS; the ongoing regulatory complexity for many cannabis-derived consumer products described by FDA; the capital intensity and operational friction common to processing startups in immature markets; and the predictable mismatch between rapid field expansion and slower downstream specification work.

What we mark as uncertain or situational: any blanket count of “failed” plants by state, uniform recovery timelines, and claims that one processing configuration (fiber-first, grain-first, extraction-first) is universally “the winner.” Those outcomes depend on contract depth, utility prices, labor pools, and local policy details beyond what a national essay can responsibly pin down.

Editorial standards

Hemp.com aims for transparency without theater. This piece uses composite industry voices—scenes and roles that are plausible because they recur in processing communities—but it does not attribute dialogue to named individuals we did not independently interview for this draft. Where evidence is thin, we say so in plain view rather than smuggling speculation inside authoritative numbers.

We avoid medical claims and legal advice. Hemp ingredients and products intersect with serious regulatory frameworks; readers making business or compliance decisions should consult qualified professionals and primary regulatory text, including the agency resources linked above.

If a reader believes we have misstated a fact, Hemp.com’s practical standard is to correct material errors promptly when verified, with a clear note of what changed. Non-material clarifications may be handled as updates in line with site policy.

Explore further

For readers building or buying in the hemp supply chain, the useful next clicks are rarely more hype—they are counterparties with audited processes, realistic MOQs, and clear specs. Hemp.com’s directory and listings exist to help operators discover each other; some entries may be commercial relationships or sponsored placements per site disclosures.

Disclosure: When this article links to off-site regulatory or educational resources, those links are for reader reference rather than endorsements. If Hemp.com earns fees from directory placements, affiliate relationships, or lead-generation products tied to categories mentioned here, that monetization should be labeled wherever the product appears, in line with Hemp.com’s monetization disclosure practices, so the editorial story and the business model do not blur.

Onward reading that pairs well with this arc includes state agriculture portals for your specific jurisdiction, equipment vendors’ maintenance realism (case studies beat brochures), and—where available—cooperative extension guidance on regional hemp markets. Those sources rarely sparkle, but they age better than keynote promises.

Find suppliers

Browse verified industrial hemp businesses in the Hemp.com directory.